Introduction

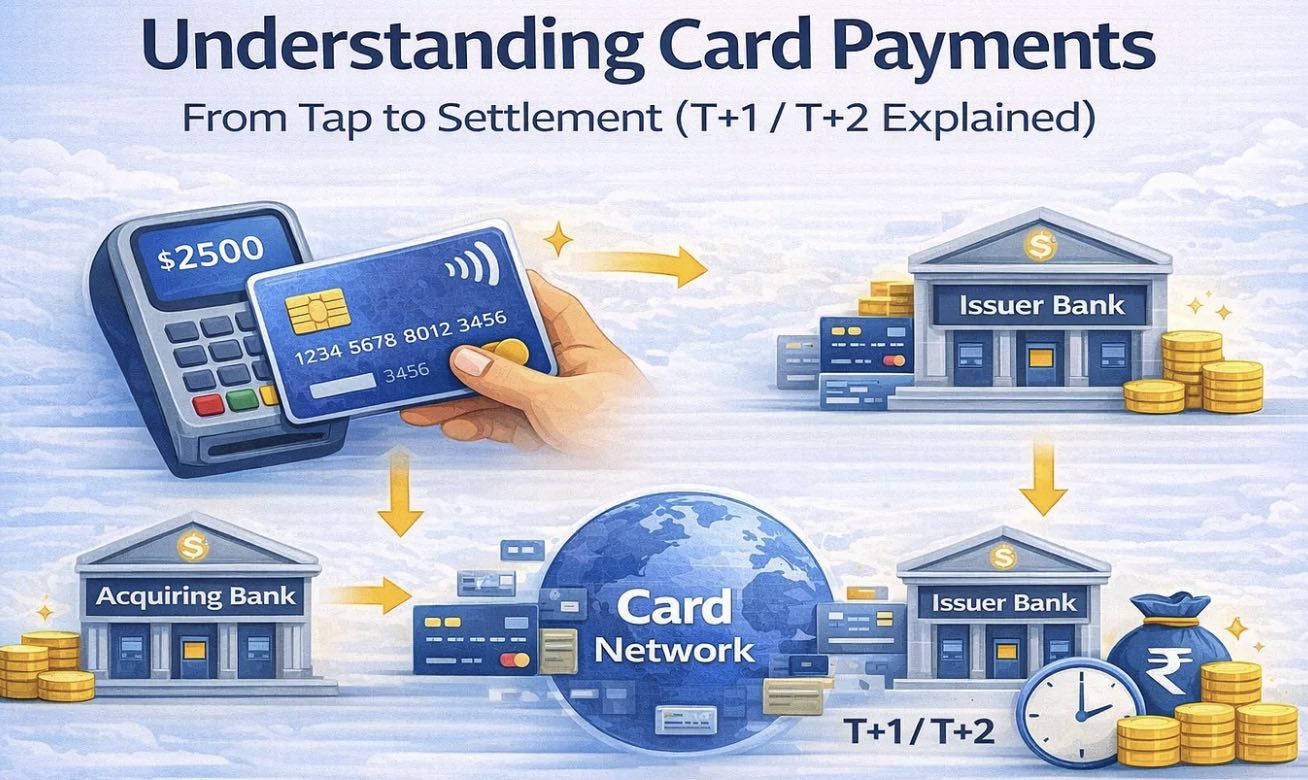

Digital payments feel instant. You tap your card or phone, see “Payment Successful,” and walk away. But behind the scenes, a card payment is a multi-step financial workflow involving banks, networks, security checks, and settlement cycles. This is why merchants usually receive money on T+1 or T+2 days, not instantly.

This article explains the end-to-end card payment flow using a simple real-world example, including who the issuer and acquirer are, how data flows, and why settlement takes time.

Context: A Simple Example

- Customer Card: ICICI Bank Credit Card

- Issuer Bank: ICICI Bank

- Merchant: Local retail store

- Acquirer Bank: HDFC Bank (The merchant’s bank)

- Card Network: Visa

- Payment Mode: Tap to Pay (Physical or Virtual Card)

Step 1: The Tap (Customer → Merchant)

You tap your contactless card or mobile wallet (Apple Pay, Google Pay, etc.) on a payment terminal.

What happens technically:

- The terminal uses NFC (Near Field Communication).

- The card or phone does not share your actual card number.

- Instead, it sends:

- A tokenized card number

- Expiry date

- A one-time cryptogram (unique for this transaction)

This makes replay attacks and data theft nearly impossible.

Step 2: Authorization Request (Merchant → Acquirer)

The merchant’s POS system creates an authorization request and sends it to the acquiring bank (The merchant’s bank).

Example (Simplified Authorization Request Payload)

{

"transactionAmount": 50.00,

"currency": "USD",

"merchantId": "M123456",

"terminalId": "T987654",

"paymentMethod": "CONTACTLESS",

"tokenizedCard": "4111XXXXXXXX1111",

"cryptogram": "A1B2C3D4",

"timestamp": "2026-01-21T10:45:30Z"

}Step 3: VisaNet Processing (Acquirer → Visa Network)

The acquirer (The merchant’s bank) forwards the request to VisaNet, Visa’s global payment network.

VisaNet performs:

- Token detokenization (secure environment)

2. AI-based fraud analysis

3. Risk scoring using:

- Spending behavior

- Device fingerprint

- Location patterns

- Merchant history

Visa’s ML systems analyze thousands of signals in milliseconds.

Step 4: Issuer Decision (VisaNet → Issuing Bank)

VisaNet sends the request to your card-issuing bank.

The bank checks:

- Available balance or credit limit

- Account status

- Risk score from Visa

- Velocity and anomaly checks

{

"authorizationResult": "APPROVED",

"approvalCode": "A76421",

"riskScore": "LOW",

"responseTimeMs": 120

}Step 5: Approval Response (Issuer → Merchant)

The approval travels back:

Issuing Bank → VisaNet → Acquirer → Merchant Terminal

The terminal displays:

“Payment Approved”

All of this typically happens in 300–700 milliseconds.

Step 6: Completion & Settlement (Post-Transaction)

Later (usually end of day):

- Merchant submits batch settlement

- Funds move from issuer to acquirer

- Merchant gets paid (T+1 or T+2)

If you have an ICICI Bank credit card, the roles are as follows in a standard card payment flow:

Issuer

ICICI Bank

- The issuer is the bank that issues the credit card to you.

- ICICI Bank provides the credit limit, generates the physical and virtual card, authorises transactions, and bills you.

Acquirer

The merchant’s bank (Acquiring Bank)

- The acquirer is the bank that provides payment acceptance services to the merchant (POS machine, payment gateway, Tap-to-Pay, etc.).

- For example, if you pay at a store whose POS machine is provided by HDFC Bank, then HDFC Bank is the Acquirer, even though your card is from ICICI.

Example (Simple Flow)

- You → use ICICI Bank credit card (physical or virtual)

- Merchant → has POS / payment gateway from another bank (or even ICICI)

- Merchant’s bank → Acquirer

- Your bank → Issuer (ICICI Bank)

- Card network (Visa / Mastercard / RuPay) → connects issuer and acquirer

Important Note

- If a merchant also uses ICICI Bank’s POS or payment gateway, then ICICI can act as both Issuer and Acquirer in the same transaction.

Why merchants get paid on T+1 / T+2 for card payments.

Merchants receive payments on T+1 or T+2 days because a card transaction is not a single instant transfer; it goes through authorization, clearing, settlement, and reconciliation steps involving multiple parties.

Below is a clear, business-level explanation.

1. What happens at the time of payment (T = Transaction Day)

When you pay using a credit card (physical or virtual):

- The issuer bank (ICICI) only authorizes the transaction.

- Authorization means:

“Yes, the card is valid and credit is available.” - No actual money moves at this stage.

This step takes seconds, which is why the payment feels instant.

2. Clearing & Settlement happen later (T+1 / T+2)

After business hours:

- The merchant’s acquirer bank batches all transactions.

- These are sent to the card network (Visa / Mastercard / RuPay).

- The network routes them to the issuer bank (ICICI).

- ICICI confirms the final amount and prepares funds.

- Money flows back through the network to the acquirer.

- The acquirer credits the merchant account.

This multi-party process typically completes in 1–2 working days.

3. Risk & Dispute Management

The delay allows time for:

- Fraud checks

- Chargeback risk assessment

- Reversals or failed transactions

- Compliance checks

This protects both banks and merchants.

4. Merchant Discount Rate (MDR) Calculation

Before paying the merchant:

- Acquirer deducts MDR (fees for network, issuer, and acquirer).

- Final net amount is credited after settlement.

If this article helped you, I’d appreciate a clap. Follow the page to stay updated with upcoming posts.